I get it—long-term care isn’t a straightforward topic to take care of. Nobody desires to consider themselves or their family members being unable to reside on their very own.

However hear me out: Although long-term care is an uncomfortable matter, it’s an excellent essential one. That’s as a result of some type of long-term care—like dwelling in a nursing residence, assisted dwelling facility, or needing in-home care—is probably going in your future, so you might want to take into consideration the way you’re going to pay for it.

My guess is you in all probability have already got some questions, like, Is long-term care insurance coverage actually vital? and How are you aware in case you really need it? You may also be questioning whether or not Medicare will cowl the prices of long-term care.

So, let’s have a look at who wants long-term care insurance coverage and the way a lot you possibly can anticipate to pay for it. That method, you possibly can put collectively a strong plan to your future.

What Is Lengthy-Time period Care Insurance coverage?

Long-term care insurance covers the associated fee for a nursing residence, assisted dwelling facility, or in-home care once you grow old and begin coping with well being points. Lengthy-term care is outlined as any care that’s longer than three months.

Lengthy-term care insurance coverage additionally covers issues like grownup day care companies, residence modifications, and care coordination (or administration). For many individuals, it permits them to guard their retirement financial savings whereas additionally dwelling of their residence longer. It’s additionally one of many eight types of insurance you want.

Who Wants Lengthy-Time period Care Insurance coverage?

In the event you’re at the moment wholesome, you is likely to be questioning, Do I would like long-term care insurance coverage? Sure! You aren’t required by any legal guidelines to buy long-term care insurance coverage, however you continue to want a coverage as a result of odds are you’ll find yourself needing long-term care—and it’s not low-cost.

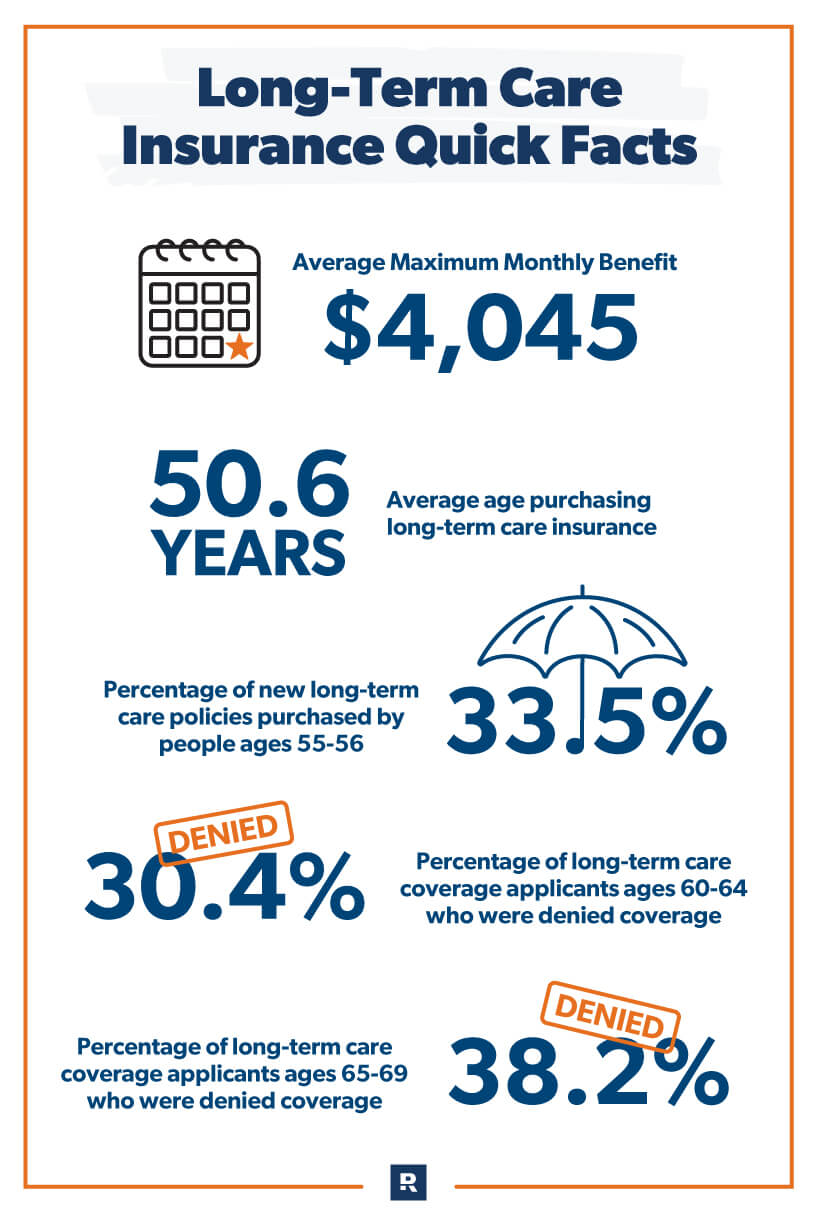

The numbers say 7 out of 10 People over 65 will want long-term care, and an estimated 20% of People will want it for longer than 5 years.1 And the standard price of simply one month in a nursing residence in the USA is $8,910!2

That’s insane, you guys. Until you’ve constructed sufficient wealth to be self-insured and pay for that price your self, long-term care insurance coverage is one of the best ways to be sure you don’t find yourself operating out of cash towards the tip of your life. Common health insurance gained’t cowl these prices, however long-term care insurance coverage will.

Now, you is likely to be questioning whether or not there are any authorities applications that may assist. Properly, for starters, Medicare will not cowl long-term care prices. And whereas Medicaid—the federal government program designed for individuals who actually don’t have any cash—will cowl some long-term care bills, it ought to by no means be your first selection since you’ll should spend all of your belongings earlier than you obtain assist.

So, in case you wouldn’t really feel comfy writing a verify for $9,000 each month for a number of years, you’ll need long-term care insurance coverage.

Milliman Lengthy Time period Care Insurance coverage Survey3

Is Lengthy-Time period Care Insurance coverage Value Shopping for?

Sure, long-term care insurance coverage is definitely worth it. Although it may be costly, most insurance policies work out to be a discount in the long term, contemplating what you get in return. The truth is, most People merely will be unable to afford the tremendous excessive prices of long-term care. Or they’ll should dip into their financial savings or retirement funds to pay for it, which is a horrible plan!

Lengthy-term care insurance coverage additionally lets you reside in your house longer as a result of it pays for issues like in-home care and residential modifications (like including a wheelchair ramp).

One other profit is that your loved ones and associates gained’t be burdened with each side of your care. You possibly can spend extra high quality time with them with out relying in your grown children or associates to return over daily to assist.

![]()

Long-term care is an important decision. Connect with a trusted pro to make sure you have the right coverage.

With long-term care insurance coverage, you’ll enter your golden years with a plan, and your high quality of life might be higher than in case you had been continuously attempting to chop prices. Your long-term care insurance coverage premiums could appear costly now, however they’ll be price it later once you begin getting these long-term care payments within the mail.

How A lot Does Lengthy-Time period Care Insurance coverage Value?

Relying on elements like your age, gender, well being and household well being historical past, the cost of long-term care insurance might be reasonably priced. For others, it may be dearer. The fee additionally varies relying on the place you reside and what sort of coverage you decide.

The common 60-year-old man pays $1,200 per yr for a coverage that covers $165,000 in care. The common 60-year-old lady pays $1,960 for a similar protection.4 (As a result of girls are inclined to outlive males, insurance coverage corporations require them to fork over extra money to make up for the added danger.) The common 60-year-old couple pays $2,550 a yr for a mixed coverage.5 The {couples} low cost ranges from 15–30%, relying on the place you reside.6

It’s additionally essential to know that long-term care insurers can improve your charges after you enroll, so don’t be stunned in case your charges climb. However right here’s a silver lining: Lengthy-term care insurance coverage premiums are tax-deductible as much as sure limits, so you may avoid wasting cash there.

When Ought to I Get Lengthy-Time period Care Insurance coverage?

I like to recommend getting long-term care insurance coverage once you flip 60. Consider it as a birthday current! (Okay, that doesn’t should be the solely current you get, however it’s an essential one.)

About 92% of long-term care claims are filed by folks older than age 70, with most new claims beginning after age 80.7 That’s why it doesn’t make sense to buy a long-term care insurance coverage coverage any sooner than age 60. You don’t need to dish out cash for an additional decade once you don’t have to.

However remember that insurance coverage isn’t one-size-fits-all. It’s essential do what’s best for you and your loved ones. In the event you or your partner has a household historical past of sickness at a younger age, or both of you’re at the moment coping with large well being points, you may have to get long-term care insurance coverage earlier. The peace of thoughts you’ll have is price greater than any money you’ll save on premiums. However don’t do it since you’re afraid of what may occur. If it’s not prone to occur, wait till you’re 60.

You might have heard you’ll pay much less and lock in a decrease premium in case you purchase your coverage at age 50, however don’t overlook that insurers can change your premium after you purchase your coverage.

Will Your Well being Have an effect on Your Capability to Purchase a Coverage or Declare Advantages Later On?

Whereas shopping for a long-term care coverage is nearly at all times a fantastic thought, not everybody qualifies to purchase it. Sadly, sure well being points make insuring some folks too costly for carriers.

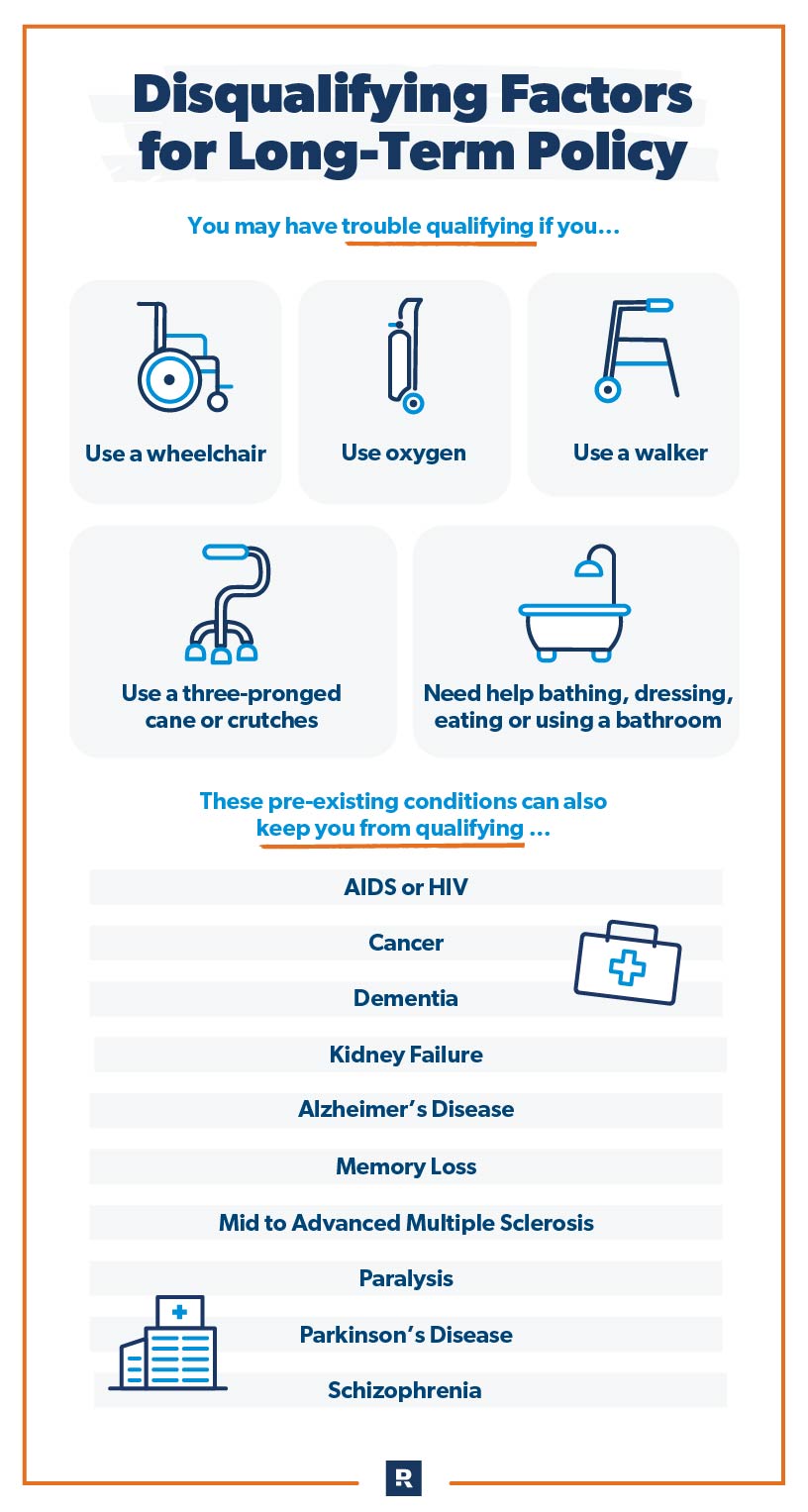

You’ll have bother qualifying in case you already:

- Use a three-pronged cane or crutches

- Use oxygen

- Use a walker

- Use a wheelchair

- Need assistance bathing, dressing, consuming or utilizing the toilet

What if You Have a Preexisting Situation?

A preexisting situation can even preserve you from having the ability to get a long-term care coverage. Here’s a record of main well being situations that disqualify folks:

- AIDS or HIV

- Alzheimer’s illness

- Most cancers

- Dementia

- Kidney failure

- Reminiscence loss

- Mid to superior a number of sclerosis

- Paralysis

- Parkinson’s illness

- Schizophrenia

What if You Have a Preexisting Situation?

A preexisting situation can even preserve you from having the ability to get a long-term care coverage. Here’s a record of main well being situations that disqualify folks:

- AIDS or HIV

- Alzheimer’s illness

- Most cancers

- Dementia

- Kidney failure

- Reminiscence loss

- Later to superior a number of sclerosis

- Paralysis

- Parkinson’s illness

- Schizophrenia

The Finest Approach to Get Lengthy-Time period Care Insurance coverage

The finest long-term care insurance coverage coverage is the one that matches your price range and covers your future wants.

Be certain that the coverage you select pays you sufficient to maintain your retirement financial savings intact. In the event you’re on a good price range, you possibly can attempt decreasing your premium by selecting an extended elimination interval (the time you need to wait between once you begin receiving long-term care and when your insurance coverage begins paying the payments)—however provided that you possibly can afford to pay for 3 months of care out-of-pocket.

One of the simplest ways to be sure you get the correct coverage, although, is to speak with an impartial insurance coverage agent. They’ll reply all of your questions, store round with a number of completely different long-term care corporations, and get you quotes that may prevent 1000’s of {dollars} and a great deal of pointless worries.

Do You Have the Proper Insurance coverage?

Take the protection checkup to seek out out what insurance coverage protection it is best to add, tweak, or drop based mostly in your particular person wants.

{kind=link}