When you’re out there for a budgeting methodology that’s the most effective on your cash, may I recommend the zero-based finances? (I would. I will.) However what makes it the most effective? And the way do you make (and hold) a zero-based finances?

Let’s reply all that. Proper now.

What Is Zero-Based mostly Budgeting?

Zero-based budgeting is when your earnings minus your bills equals zero. Good title, proper?

So, in the event you make $5,000 a month, the whole lot you give, save or spend ought to add as much as $5,000. Each greenback that is available in has a objective, a job, a objective. Nothing is left hiding or getting mindlessly spent on grande, no-whip, half-caff, white chocolate mochas with a single pump made with soy. You realize what? Scratch that. Coconut milk. You’re doing full keto, bear in mind?

However I need to be clear: A zero-based finances doesn’t imply you could have zero {dollars} in your checking account. It simply means your earnings minus all of your bills equals zero. Maintain your self somewhat buffer of $100–300!

Easy methods to Make a Zero-Based mostly Price range

Earlier than you begin making your zero-based budget, log in to your checking account or seize these financial institution statements out of the drawer you shoved them into considering, I’ll want that sooner or later. (Guess what: At some point is right here!) Having this in entrance of you’ll come in useful while you’re questioning how a lot you usually make or spend on stuff. You may also try these budget percentages and averages in the event you’re questioning what the standard family is spending.

Okay, right here’s easy methods to do a zero-based finances:

1. Checklist your month-to-month earnings.

After all you are able to do this the old style means with a sheet of paper, however I like to make use of EveryDollar. (Belief me, the maths that’s developing is means simpler with our free budgeting app.)

What counts as earnings? Your common paychecks and something further you intend to herald through the month, like all that money out of your facet hustle as a pizza supply driver or weekend balloon artist for teenagers’ events. Write all of it down and add it up! That’s your whole month-to-month earnings, aka what you’ve set to work with this month.

P.S. If you wish to begin getting your numbers down with our budget template after which swap over to EveryDollar, that’s cool too.

2. Checklist your bills.

Okay, now you understand what’s coming in—so it’s time to plan for what’s going out. Consider the whole lot you spend cash on through the month. And I imply the whole lot. Checklist out your bills like this:

- Giving (This must be 10% of your earnings.)

- Financial savings (This depends upon your Child Step, which I’ll clarify in a second.)

- The 4 Partitions (These are the highest bills to cowl: food, utilities, shelter and transportation.)

- Different necessities (I’m speaking about insurance coverage, debt, childcare, and so forth.)

- Extras (Right here’s the enjoyable half: leisure, enjoyable cash, eating places—you get the concept.)

- Month-specific bills (Plan for any holidays, celebrations or semiannual bills due this month.)

Professional tip: Don’t neglect to provide your self a miscellaneous class too so that you’ve acquired somewhat further cushion in your spending. That means, something that pops up unexpectedly isn’t an issue—it’s within the finances.

Double professional tip: While you’re placing bills within the finances, begin with wants (these 4 Partitions) earlier than needs (like enjoyable cash).

3. Subtract your bills out of your earnings to equal zero.

While you subtract all these bills out of your earnings, it ought to equal zero. When you don’t hit zero at your first go, welcome to the bulk! Yep, that’s proper. Virtually nobody will get this proper the primary time. That. Is. Fantastic. However let’s discuss easy methods to repair it!

![]()

Start budgeting with EveryDollar today!

Obtained cash left over? First, throw some confetti and do a celebration dance. (Or in the event you’re like me and might’t dance to save lots of your life, a hearty fist pump will do.) Then, put that cash to work!

The place?

In your present Child Step!

What’s that?

I instructed you I’d come again to this. It’s definition time: The 7 Baby Steps are the confirmed, guided path to save cash, repay debt, and construct wealth (aka win with cash). They’re the seven cash objectives that can take you from the place you might be to the place you need to be. Placing your cash right here offers you probably the most bang for these leftover bucks.

However what occurs in the event you don’t have cash left over? Let’s discuss what to do in the event you subtract your deliberate bills and find yourself with a detrimental quantity. This implies you’re spending greater than you make, and that simply received’t work. However don’t freak out. You can get the quantity to zero.

Get out your metaphorical hedge clippers, and trim that finances. You possibly can decrease your deliberate spending quantities the place you’re ready or cut some spending out utterly. (FYI, begin with the restaurant line! Then take up meal planning to save lots of on groceries and hold from being tempted to hit the drive-thru every evening.)

You may also up your earnings by beginning a side hustle, promoting stuff, or discovering another approach to make more money. (When you aren’t already a weekend balloon artist, it might be time to start out. Heck, possibly you’re taking this gig into weeknights for much more further earnings.)

That’s it for making the zero-based finances, however I’ve acquired two extra steps that’ll make it easier to truly stick with it.

4. Observe your bills (all month lengthy).

So, you’ll be able to’t simply arrange that finances and go away it. That will get you actually nowhere together with your cash. You’ve acquired to get in there and track your transactions. Each single one. Which means any cash that is available in or goes out will get put into the best finances line.

While you make $100 out of your facet hustle, add that cash to your earnings class. While you pay the lease, subtract that expense from housing. While you refill the fuel tank, subtract that from the fuel finances line underneath transportation.

That is the way you keep on prime of your spending. That is how you retain from overspending.

By the way in which, you’ll be able to streamline this course of with the premium version of EveryDollar. You’ll join your financial institution to your finances so transactions stream proper in. Then, you simply have to pull and drop them into place!

5. Make a brand new finances (earlier than the month begins).

Whereas it’s true your finances received’t change a ton month after month, it’s going to change some. So, create a brand new zero-based finances each single month. Bear in mind these month-specific expenses I discussed within the second step? That is the place they actually come into play.

Additionally, do that earlier than the month begins so that you’re prepared, forward of time, for what’s coming your means.

By the way in which, if you would like some extra data on easy methods to begin, mess around with our Budget Calculator.

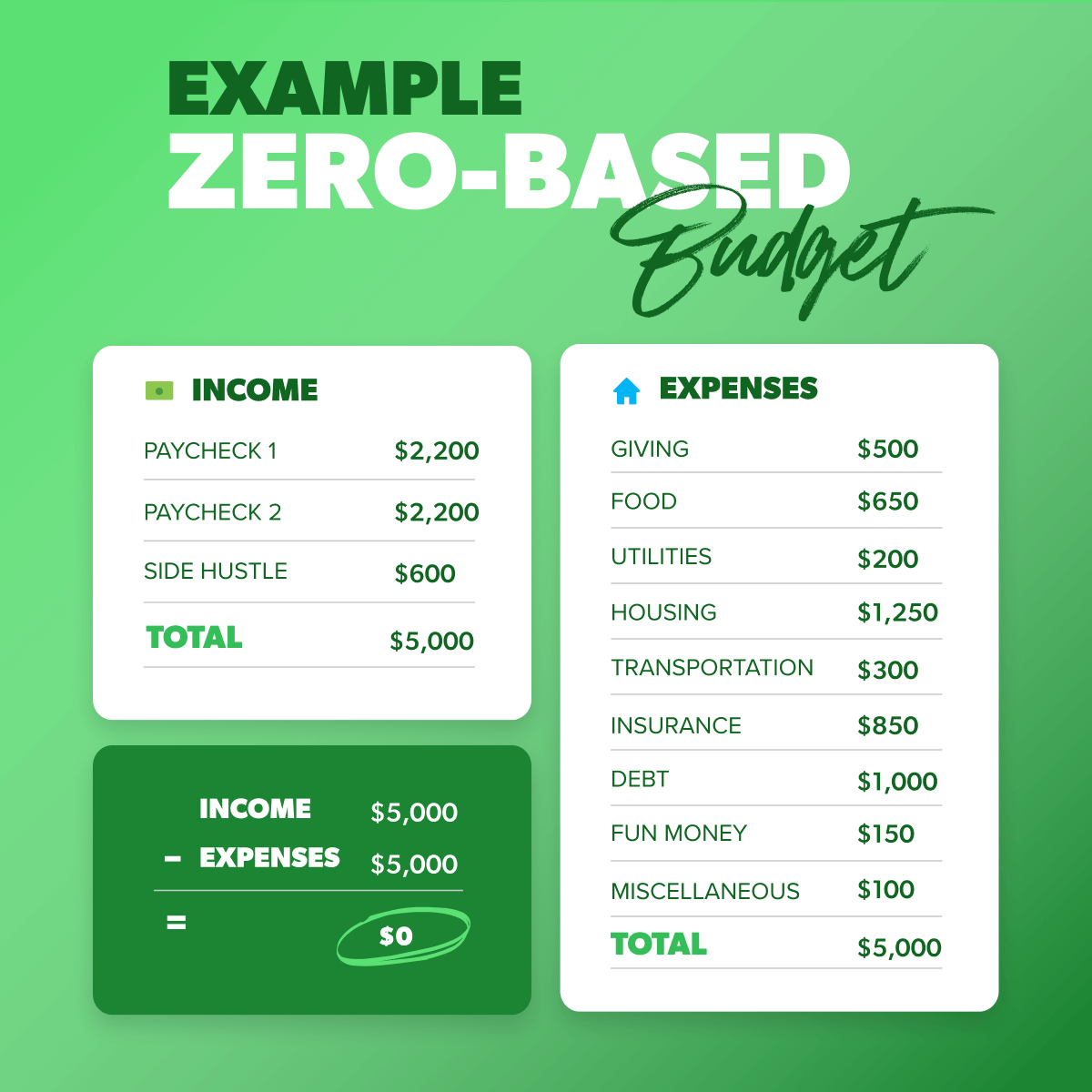

Instance of a Zero-Based mostly Price range

Right here’s a brilliant fundamental instance of a zero-based finances so you’ll be able to see how the maths works out.

Benefits of Zero-Based mostly Budgeting (Over Different Budgeting Strategies)

1. 50/30/20 Rule

The 50/30/20 budgeting rule follows these percentages: 50% of your earnings goes towards your wants, 30% goes towards needs, and 20% goes towards financial savings. After all it’s good to have some numbers that can assist you begin budgeting, however these numbers go away lots to be desired. And I imply lots.

To start with, in the event you’re utilizing our Child Steps (which you actually ought to), you aren’t all the time placing cash towards financial savings. You’re taking your objectives one (child) step at a time. That sort of focus brings fast wins and lasting wealth.

Second, the 50/30/20 rule lumps debt into wants—however requires you to make minimal funds solely. You possibly can’t make most progress with minimal funds.

Third, these three percentages keep the identical irrespective of the place you might be in life. When you’ve acquired a ton of pupil mortgage debt—50/30/20. When you’re debt-free and investing in retirement—50/30/20.

And eventually, while you do the maths on common earnings minus common bills, the common American spends far more than 50% on wants. It’s extra like 80%. This methodology doesn’t even work, folks. (My Sensible Cash Blissful Hour co-host and good friend Rachel Cruze breaks down the maths on that and the whole lot else concerning the 50/30/20 rule, in the event you’re .)

2. 60% Answer

Within the 60% answer methodology, you cowl all of your wants and needs with 60% of your finances. The opposite 40% is for saving. Then, that 40% will get divided up into three financial savings classes (10% for retirement, 10% for long-term financial savings, 10% for short-term financial savings) with 10% left for “enjoyable.”

To start with, that’s plenty of dividing. Second, I like financial savings—however in the event you’ve acquired debt, you shouldn’t be placing 40% of your cash into financial savings. Try to be destroying that debt. Hardcore. And after that, you must put as a lot as you’ll be able to into constructing your fully funded emergency fund. And after that, you must make investments 15% in retirement.

Additionally, bear in mind—the common American is spending round 80% on wants. The 60% answer math doesn’t work. And this methodology simply doesn’t account for each budgeter’s particular person scenario.

3. Reverse Budgeting

Many budgeting strategies have you ever put aside cash for spending first and financial savings second. With reverse budgeting, it’s the alternative. (Therefore the title.)

On this methodology, you set your finances for saving and investing first. You then put the whole lot else in there (like housing, fuel, meals, insurance coverage, debt and the nonessentials).

So, I like the emphasis on financial savings not being an afterthought! As a result of it’s truthfully fairly simple to neglect about it.

However once more, this methodology locks you into a technique which may not match the cash objective you’re in the course of! When you’re on Baby Step 2, you aren’t considering financial savings first. You’re centered on kicking debt out of your life without end.

4. Set It and Neglect It

Okay, you’ve acquired to start out someplace with a finances. When you’ve by no means made one, getting all of your numbers down (earnings and bills) is your first step. However you don’t cease there. You don’t simply go away these numbers on the web page and hope you’ll live by them.

That is the “set it and neglect it” budgeting methodology. And it actually doesn’t work. It helps you see the place your cash ought to go—but it surely doesn’t make you accountable for the place it truly goes. And it’s a good way to overspend. No, thanks.

5. Zero-Based mostly Budgeting

You possibly can in all probability see why I’m such an enormous fan of zero-based budgeting. It’s far more customizable for the place you might be in your life. You get to determine how a lot to place towards debt, financial savings, retirement, and the whole lot else. Each. Single. Month.

You may also adapt your zero-based finances as you undergo the Child Steps. That’s what it’s made for! Each single greenback is working for you. At all times.

Can You Make a Zero-Based mostly Price range With an Irregular Revenue?

Why, sure. Sure, you’ll be able to! In case you have an irregular income (which means your earnings isn’t the identical every paycheck or comes at totally different occasions within the month), you’ll be able to nonetheless use zero-based budgeting. It’ll simply look somewhat totally different for you.

- While you’re itemizing your earnings, discover out what you’ve made the previous couple of months. (That is one other place your financial institution statements are useful.)

- Take the lowest quantity you made in that point and listing it within the finances as this month’s deliberate earnings.

- You possibly can alter the earnings later within the month in the event you make extra.

While you’re itemizing your bills, observe the listing from earlier. Simply know that the extras may need to attend till you understand you can afford them. Cowl a very powerful issues first. When you receives a commission greater than you deliberate, perform a little fist pump—then add that more money to your Child Step or one other finances line.

You should use our Irregular Income Budget Planning form to get began!

So, Why Is Zero-Based mostly Budgeting Vital?

Right here’s the deal. If you wish to make any progress together with your cash, you have to make a monthly budget. Individuals say budgeting takes them from questioning the place their cash went to telling it the place to go. That. Is. Empowering.

And a zero-based finances? Even higher. Since you’re telling each single greenback the place to go. You’re employed laborious on your cash—all of it. So all of it ought to work laborious for you.

And don’t neglect EveryDollar—the free approach to create your zero-based finances. You make the cash, and it does the maths. What a lovely relationship.

Pay attention: No matter your money goal, no matter your Child Step, wherever you might be in your private finance journey—a zero-based finances is what is going to get you (and hold you) shifting ahead.

{kind=link}