Mother or father. The official definition must be: “Caretaker of kid. Synonyms: nanny, tutor, launderer, chauffeur, coach, nurse, therapist, chef, hand-holder, tear-wiper, picker-upper, fight-breaker-upper, bottom-pamperer . . .”

It’s a wealthy and rewarding function, however the parenting duties by no means appear to cease!

This definition particularly applies to a stay-at-home mum or dad (SAHP). Whereas SAHPs might not pull down a six-figure revenue from a nook workplace, they do present rather a lot of helpful companies for the household.

Let’s discuss why stay-at-home mother and father want life insurance coverage, how large that coverage must be, and what households ought to do with the life insurance payout if the unimaginable occurs.

Understanding the Worth of a Keep-at-Residence Mother or father

The entire level of life insurance is to switch your revenue so your loved ones can operate if one thing occurs to you—so getting life insurance coverage for fogeys who usher in an revenue is apparent.

However what about protection for stay-at-home mother and father? Why do SAHPs even want term life insurance in the event that they don’t technically make an revenue? (That’s rhetorical.) It’s due to the high-dollar companies they supply!

Listed here are some of the roles a stay-at-home mum or dad covers:

- Trainer

- Childcare supplier

- Chef

- Chauffeur

- Housekeeper

- Laundry employee

- Tutor

- Coach

- Undertaking supervisor

Working a family is rather a lot like attempting to herd a litter of kittens—with out a SAHP, it’d all get ugly in a rush. If one thing horrible had been to occur to the mum or dad at dwelling, who would maintain these wants? The surviving partner can’t stop work—they nonetheless have to carry dwelling an revenue. That’s the place time period life insurance coverage is available in.

Do Keep-at-Residence Mother and father Want Life Insurance coverage?

A life insurance policy for a stay-at-home mum or dad doesn’t substitute their revenue—it gives the cash essential to cowl all the roles the SAHP did earlier than they handed away.

Clearly, it’s not possible to switch a mum or dad. Nothing will ever fill that gap within the household. However with the cash from a life insurance coverage payout, the surviving partner can rent somebody to cowl most of the obligations the SAHP used to deal with.

It’s a matter of retaining your loved ones going within the worst of conditions. Life won’t ever return to regular, however by hiring folks to assist fill within the gaps (at the least quickly), you can also make certain no person’s wants fall by means of the cracks. And that’s what issues, proper?

When Ought to You Get Life Insurance coverage as a Keep-at-Residence Mother or father?

In case you’re contemporary out of school and don’t have debt, you don’t want life insurance coverage fairly but. However for those who’re married and children are on the horizon, it’s good to go forward and buy life insurance now.

By getting life insurance coverage immediately, you’ll be lined irrespective of how lengthy it takes for that baby to come back alongside. In any case, they have a tendency to reach on their very own schedule—and infrequently sooner than you’d deliberate!

How A lot Life Insurance coverage Do Keep-at-Residence Mother and father Want?

Right here’s the large query is: how much term life insurance must you buy for the stay-at-home mum or dad? There’s no one-size-fits-all reply to this as a result of each household is totally different, however a common rule is to get a 15- to 20-year coverage of at the least $250,000–400,000.

![]()

Compare Term Life Insurance Quotes

Whenever you’re younger, getting extra life insurance coverage isn’t that costly, so it’s okay to get greater than you assume you want. After these 15 or 20 years, the children ought to all be grown and out of the home, so there’s no want for protection. To get an thought of how a lot protection you want, take a look at our term life calculator.

Protection Issues for Keep-at-Residence Mother and father

As you’re deciding how a lot protection to purchase, it’s worthwhile to assume by means of 5 main areas: household dimension, profession plans, childcare, schooling and family duties. Every of these particulars has an influence on how a lot life insurance coverage you’ll want for your loved ones.

What number of youngsters do you will have?

Greater households have larger monetary wants—from the price of childcare and groceries to paying for holidays and all of these extracurricular actions. So extra children means you’ll want a bigger life insurance coverage coverage for the SAHP.

Will the stay-at-home mum or dad be going again to work?

We’ve already touched on the high-dollar worth of the work a SAHP does (and we’ll do the maths within the subsequent few sections). However past what they contribute at dwelling, there’s additionally the chance they’ll return to work.

If that’s a part of your SAHP plan, it’s all of the extra cause to get them life insurance coverage. Sooner moderately than later, you’ll wish to purchase a coverage that’s 10–12 occasions their anticipated revenue. Then they’ll be lined both means—whether or not they’re doing the SAHP factor or going again to work. Since the price of life insurance coverage will increase as you grow old, don’t wait till the SAHP returns to work to get their coverage. Lock in a pleasant low charge proper now.

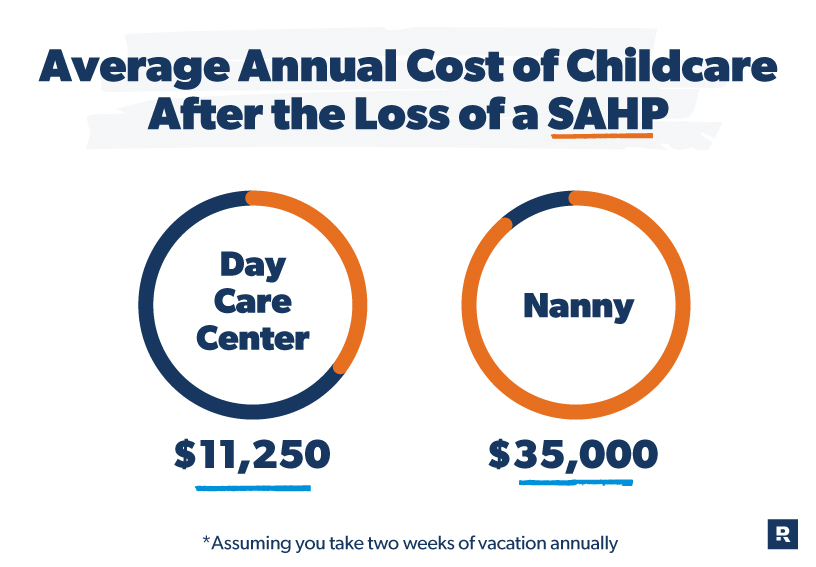

How a lot will childcare value?

If one thing occurs to the SAHP, how a lot cash would it’s worthwhile to cowl childcare bills? In line with Care.com, childcare for an toddler prices about $225 every week for a day care middle and $700 every week for a nanny.1

So, 52 weeks of care (as a result of—gross as it’s—it’s a must to pay for day care even on days your child isn’t there) might run between $11,700 and $36,400. And that’s only for one youngster. In fact, these prices differ relying on the place you reside, however you get the thought.

How a lot will schooling value?

Plenty of households select to homeschool their youngsters. If that’s the case in your loved ones, you and your partner have to determine the place the children will go to highschool if one thing occurs to the SAHP.

If you wish to go the personal faculty route, you’ll have to consider these prices. The nationwide common for personal faculty tuition is about $12,167 a yr.2 Once more, that’s only for one youngster. And that doesn’t embody all the additional prices—like provides, charges and extracurriculars.

Who will tackle family duties?

Who’ll be liable for cleansing the home if one thing occurs to the stay-at-home mum or dad? In case you simply paid somebody for fundamental housekeeping, it’d value you about $14 an hour.3 (In fact, there’s much more to working a family than fundamental cleansing—every other chores you want achieved will solely drive the invoice larger and better.) And that’s a mean, so for those who reside in California or New York, you will have to supply up the occasional arm or leg to pay for these prices.

Bear in mind, how a lot life insurance coverage you get for the SAHP will rely upon your loved ones’s wants.

As you’ll be able to see, the sensible value of what a SAHP offers their household is big! And life insurance coverage protection can provide SAHP households some actual peace of thoughts that these duties shall be nicely lined it doesn’t matter what.

We’ve heard from loads of glad prospects in our Ramsey Child Steps Group Fb group who purchased life insurance coverage for a SAHP. Take it from stay-at-home mother Vanessa D.: “We homeschool our 4 children. If I used to be to die, I’d need my husband to have the ability to proceed that. For this reason we’ve $750,000 on me. It will cowl the price of the home and sufficient for school too. Hubby has a pension and VA incapacity and will reside off of that.” Nice considering, Vanessa!

And take a look at Micaylee N.’s testimony. She is aware of the worth of her husband’s SAHP contribution: “My husband is a stay-at-home dad, and we’ve a $700,000 coverage on him.” Good for you guys, Micaylee!

Each households worth their stay-at-home mum or dad sufficient to know that if the worst had been to occur, it might value a complete lot to pay for the various jobs they do on a weekly foundation. In order that they’ve purchased insurance policies value 10 occasions the quantity they’d pay to cowl the work the SAHP does in a yr.

Now Vanessa’s and Micaylee’s households have the peace of thoughts understanding that if something occurred to their SAHPs, the surviving mum or dad might work with a financial advisor to place the life insurance coverage payout in an excellent mutual fund. (And simply so you recognize, a life insurance coverage profit is almost never taxable.)

Every year, they may use the expansion from that mutual fund (which might be round 10% a yr) to pay for the prices of childcare, meal prep, home cleansing and the opposite jobs their SAHP used to deal with.

Your personal life insurance coverage wants will rely rather a lot on the components we outlined above, however let’s take a look at Vanessa’s state of affairs for example. Her coverage is $750,000—so that might give her household a payout of $75,000 a yr (that 10% of annual development we talked about earlier) to get every little thing lined.

And the way’s this for a life insurance coverage endorsement from Melissa B.? “Begin with Zander. We did and it was very reasonably priced.” We couldn’t agree extra, Melissa!

Get the Proper Life Insurance coverage in Place As we speak

Keep-at-home mother and father usually decrease the monetary function they play of their household. Don’t make that mistake, particularly in terms of life insurance coverage! No one might ever take the place of your loved ones’s stay-at-home nurse-chauffeur-coach-therapist-hugger—nevertheless it is essential for your loved ones to have the cash they’ll have to maintain your most simple duties.

We suggest working with our RamseyTrusted associate Zander Insurance coverage. They’ll store the highest insurers available on the market and enable you get one of the best protection for your loved ones. Be sure that your wants are met by getting the proper life insurance coverage for each mother and father.

Be taught the Smarter Strategy to Do Life Insurance coverage

Life insurance coverage can really feel freakin’ complicated. Signal as much as get Ramsey’s no-nonsense recommendation, together with free entry to Dave’s video from Monetary Peace College (usually $80), plus guides and sources despatched proper to your inbox.

{kind=link}