Medical insurance is sophisticated stuff—premiums, deductibles, coinsurance, bronze, silver, gold plans (what is that this, the Olympics?!). Then throw in HSAs, HMOs, PPOs . . . what?! Attempting to determine it out will be robust.

If all these phrases have you ever scratching your head, questioning how medical insurance works, don’t fear. We’ve obtained your again.

We’ll break down precisely how medical insurance works. As a result of it’s a heck of so much simpler to get the suitable protection when you truly perceive it.

What Is Well being Insurance coverage?

Medical insurance is a technique to pay for the prices of well being care by transferring danger to an insurance coverage firm. When you pay your deductible, the insurance coverage firm will cowl some or your entire care. This fashion you gained’t end up drowning in medical payments and dealing with monetary smash.

Whereas there are a boatload of various sorts of plans, there are actually solely two important forms of medical insurance—non-public and public. Each plan falls beneath considered one of these.

Non-public protection is the type you get by way of your employer, union or the armed forces. It’s also possible to purchase it by yourself by way of the federal government’s market—Healthcare.gov—however solely throughout a sure time of yr referred to as open enrollment.

Public insurance coverage is supplied by the federal government. Assume Medicare (for these 65 years or older), Medicaid (for low-income households) or care from the Division of Veterans Affairs.

Primary Well being Insurance coverage Phrases

Since there’s virtually a medical insurance time period for every letter of the alphabet, listed here are some definitions that can allow you to higher perceive how medical insurance works.

Your premium is the quantity you pay month-to-month (typically yearly) for protection.

Your deductible is the quantity it’s important to hand over earlier than your insurance coverage cash kicks in. For instance, in case your deductible is $3,000, you’d should pay $3,000 for care earlier than your insurance coverage firm ponies up.

Your most out-of-pocket prices are the max of what you’ll pay in a given yr. So in case your plan’s most out-of-pocket prices are $6,000, when you pay that quantity, your insurance coverage pays every part over that in the remainder of the yr.

Coinsurance is said to the utmost out-of-pocket prices. It’s a technique to cut up the prices of medical companies together with your insurance coverage provider after you’ve hit your deductible.

Your copay is a set quantity you pay for issues like physician’s visits or different companies. It applies even earlier than you hit your deductible. As an illustration, in case your copay is $20 to see a health care provider about that bug that flew in your ear, and now you’re listening to a continuing buzzing noise, you’ll solely pay $20. The insurance coverage provider will cowl the remaining. Good!

Lined prices are companies your insurance coverage firm will assist pay for. Assume physician’s visits, checks, preventative care, and many others.

And that is solely the tip of the medical insurance iceberg (loopy, proper?). There’s a ton of different phrases—HMO, PPO, HDHP, HRA and HSA, simply to call a couple of. We gained’t get into all of them right here (you’re welcome), however you possibly can undoubtedly dig into these plans subsequent time you’re in search of some mild seashore studying . . .

Who Wants Well being Insurance coverage?

Everybody. For those who’re alive on Planet Earth, you want some type of medical insurance. It’s one of the best ways to guard your self from the monetary issues that may simply occur because of sudden medical occasions. Nobody’s completely resistant to severe medical conditions. That’s why health insurance is a must.

You and your loved ones want that further layer of safety. It’s like protecting an umbrella within the automobile for wet days. Most instances you don’t want it. However when it does rain, it actually is useful. Actually, medical payments are the primary trigger for chapter in America. It’s very easy to rack up lots of of 1000’s of {dollars} in medical bills.

Even when you’re unemployed, you continue to have choices like COBRA insurance to be sure you’re coated. And when you’re self-employed, you gained’t be capable to get an employer plan, however you possibly can nonetheless purchase protection by yourself.

The underside line? No matter your state of affairs, you want medical insurance. Interval. Full cease.

How Does Well being Insurance coverage Work?

So, how does medical insurance work?

First, you pay a month-to-month premium to your insurance coverage firm. They then comply with pay for any medical prices you may want all year long—however solely after you pay your deductible. So it doesn’t matter what, you’re going to have some out-of-pocket prices.

If you wish to pay fewer out-of-pocket prices, you possibly can go along with a decrease deductible—however you’ll pay the next month-to-month premium. And vice versa, if you wish to pay a decrease premium—much less per thirty days—you possibly can go for the next deductible.

When you hit that deductible, you possibly can file a claim. If it’s coated, your insurer will cowl the prices of the care. In the event that they deny your declare, you possibly can attraction it. Worst-case state of affairs, you’ll should cover the costs on your own.

One other factor to bear in mind is that, relying in your plan, it’s possible you’ll be restricted to a sure community of suppliers. Some plans don’t allow you to merely use any physician you need. It’s important to work within a longtime community.

What Does Well being Insurance coverage Cowl?

Medical insurance helps cowl many of the prices of medical care. Issues like pharmaceuticals, hospital stays, emergency care, preventive and non-preventive care, common physician’s visits, and different medical companies like X-rays, CT scans or assembly with specialists (relying in your plan). And do not forget that a few of this care solely kicks in after you’ve met your deductible.

Due to modifications from the Reasonably priced Care Act (ACA), medical insurance has to cowl not less than these 10 important companies:

- Preventive care—like routine checkups for you or your youngsters

- Hospitalization

- Lab checks—suppose blood work

- Being pregnant, maternity and new child take care of that new toddler

- Emergency room care—relying on the circumstances, your insurance coverage may nonetheless cowl this if it’s out of community.

- Psychological well being, substance-abuse companies

- Rehabilitation companies

- Outpatient care—service you get if you don’t have to remain on the hospital

- Pediatric companies (together with oral and imaginative and prescient care)

- Prescribed drugs1

One other change because of the ACA is that insurance coverage corporations are now not allowed to disclaim you based mostly on preexisting circumstances. So in case you have diabetes, you’ll now be capable to get coated.

What Does Well being Insurance coverage Not Cowl?

There’s at all times a catch, isn’t there? Medical insurance isn’t a magic bullet that addresses each doable factor that might go fallacious. There are some issues it often doesn’t cowl.

Listed here are a couple of examples:

- Cosmetic surgery—Sorry, your insurance coverage gained’t cowl that nostril job you’ve at all times dreamed of.

- Different or homeopathic drugs like acupuncture, therapeutic massage or naturopaths.

- Experimental stuff—If there’s new know-how on the market that your physician is recommending, it most likely gained’t be one thing your provider will cowl. Simply verify upfront to see if it’s an choice.

- Lengthy-term care—An enormous false impression about medical insurance is that it covers long-term care. It doesn’t. And this delusion could cause actual issues since long-term care is so pricey.

- Elective surgical procedure—These are issues you may want completed however your physician can’t show you want.

- Weight-loss surgical procedure—Though some plans do cowl this if it’s deemed medically crucial, most instances you’ll should pay for this out of pocket.

- Medical care that’s unapproved—This implies you didn’t get the sign-off out of your well being insurer earlier than you bought the care. Professional tip: Examine together with your insurance coverage firm earlier than you get the medical care to ensure they’ll cowl it.

The ethical of the story? Fastidiously learn your Abstract of Advantages Protection to verify that no matter medical care you want is truly coated. And attain out to your insurance coverage firm to double-check.

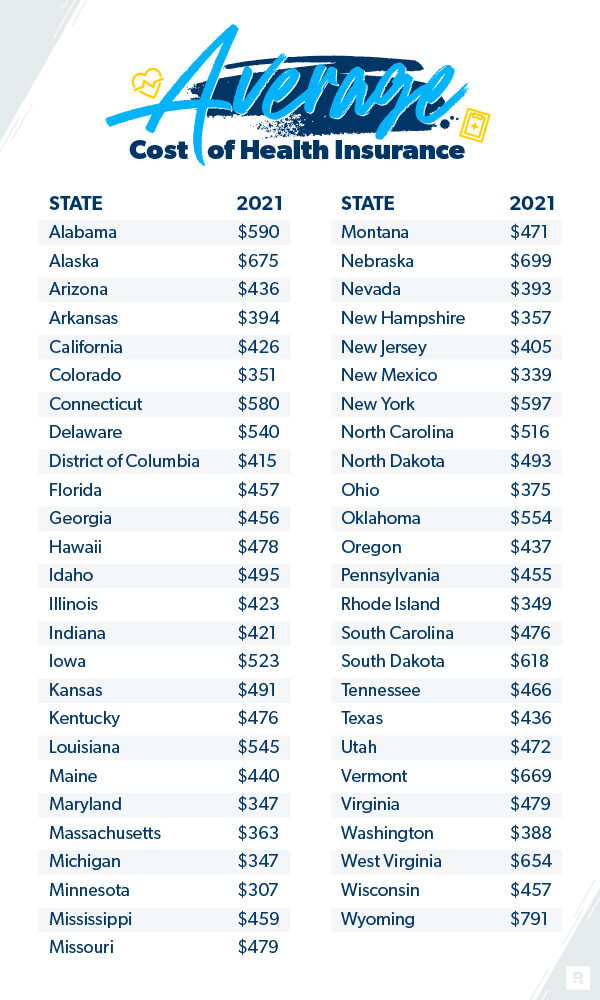

How A lot Does Well being Insurance coverage Value?

The cost of health care insurance varies fairly extensively and will be arduous to pin down. However there may be some information on it.

The typical American pays $452 per thirty days for market medical insurance.2 The typical household can count on to pay $1,779 per thirty days.3

And if it looks like well being care insurance coverage is getting dearer, it’s as a result of it’s. Over the past decade, prices have risen considerably. For instance, the common household is paying 55% extra of their premium in 2020 versus 2010 in keeping with the Kaiser Household Basis.4 And that quantity is up 22% since 2015.5 However premiums have solely risen 4% when evaluating 2020 in opposition to 2019.6

Well being care prices are based mostly on a ton of various components—issues like your age, how many individuals are in your plan, your degree of protection, the place you reside and who your employer is. A few of these issues aren’t in your management, however some are.

There are some issues you are able to do to save money in your medical insurance premiums. And as we noticed earlier, if you wish to pay much less now (however extra later), go for a decrease premium and better deductible. For those who’d fairly pay extra up entrance, pay the next month-to-month premium and a decrease deductible.

A Well being Plan Instance

So, we’ve dug into the medical insurance phrases, damaged down how medical insurance works, and discovered what’s and isn’t coated. Now we’re prepared to take a look at a couple of actual numbers. Medical insurance could make an enormous distinction in overlaying life’s sudden occasions and protecting you out of medical debt.

Let’s fake you bought in a severe automobile accident (I do know, it’s not enjoyable to consider however bear with us).

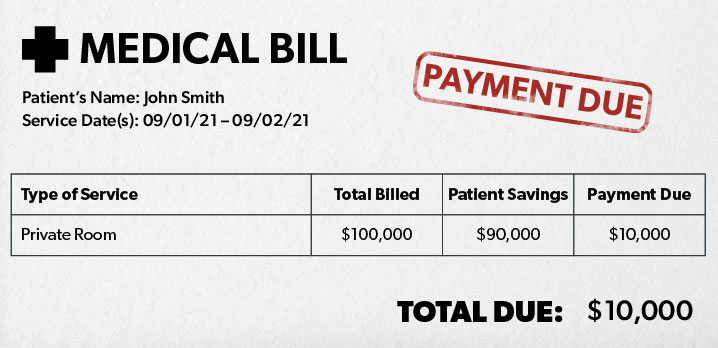

You get residence from the hospital after making a speedy restoration (nice job!). You open your mail. You’re pondering the invoice may be perhaps round $10,000. Perhaps $20,000 tops. Nope. A whopping $100,000. What?! However I used to be solely within the hospital for 2 days, and the meals wasn’t even that good.

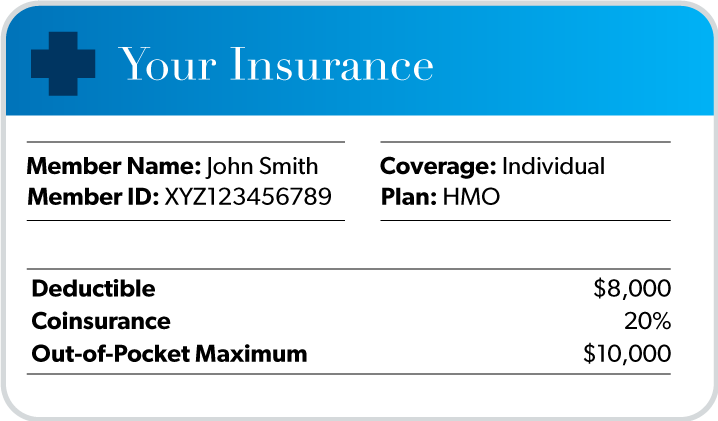

Fortunately you thought forward for moments like this. You will have stable medical insurance protection in place. Right here’s what it seems to be like:

- Your deductible: $8,000

- Your coinsurance: 20%

- Out-of-pocket most: $10,000

Assuming your care was from docs and hospitals that have been inside your insurance coverage firm’s community, right here’s what occurs to that $100,000 invoice.

Assuming your care was from docs and hospitals that have been inside your insurance coverage firm’s community, right here’s what occurs to that $100,000 invoice.

First, it’s important to pay the $8,000 to fulfill your deductible.

Subsequent, you’re going to wish to pay 20% of the prices till you hit your out-of-pocket most. So that you’ll find yourself paying one other $2,000 till you hit that $10,000 restrict.

However right here’s the nice half. Though you simply spent $10,000, your insurance coverage firm will (lastly) kick in and canopy the remainder of the invoice.

So right here’s the abstract of what you’d find yourself paying in whole after the $100,000 occasion:

Complete value of medical care: $100,000

Your share: $10,000

Your insurance coverage firm’s share: $90,000

It’s apparent simply how useful medical insurance will be in instances like this. With out it, you’d be caught with that $100,000 invoice. Not good.

It’s apparent simply how useful medical insurance will be in instances like this. With out it, you’d be caught with that $100,000 invoice. Not good.

What Are the Advantages of Well being Insurance coverage?

Though it’d seem to be a ache, there are numerous advantages to medical insurance.

Listed here are just some:

- You’ll get monetary savings. Medical insurance helps offset what can typically be sky-high well being care prices. You gained’t be caught paying for each penny out of pocket.

- Entry to a Well being Financial savings Account. Sure plans will let you put cash in a pretax account referred to as a Health Savings Account (HSA). HSAs are like a superpower in relation to paying for medical bills. If you will get one, you must.

- You’ll be more healthy. Having medical insurance—with usually no out-of-pocket prices for preventive care—will imply you’ll catch well being points early on.

- Peace of thoughts. You’ll sleep higher understanding you and your loved ones are protected if one thing sudden occurs.

- Keep away from monetary smash. Medical insurance will preserve you out of chapter or combating hospitals over lots of of 1000’s of {dollars} in medical care. Yuck!

What’s the Finest Approach to Get Well being Insurance coverage?

There are a pair other ways to get medical insurance. First, you should buy it by way of your employer’s plan. Typically it’s cheaper to purchase it this fashion since they’ll get a reduction from shopping for in bulk. However this isn’t at all times the case. It is best to contemplate different choices as a substitute of simply mechanically signing up for an employer’s plan.

One other means is thru the federal government market. Round 175 insurance coverage corporations supply packages there. And relying in your revenue, you can qualify for presidency tax incentives that can deliver down the price of your premiums. A 3rd means is to purchase it straight from medical insurance corporations.

Lastly, since medical insurance will be tremendous sophisticated, it may be arduous to determine the most effective plan for you and your loved ones. You don’t need to overpay or underpay. That’s why put collectively an inventory of proactive subsequent steps you possibly can take in the present day to know what’s greatest for you and the best way to get the suitable protection in place.

{kind=link}